United States X-ray Market Overview

The United States X-ray Market represents one of the most advanced and structurally stable diagnostic imaging markets worldwide. As a key regional contributor to the broader Global X-ray System Market, the United States maintains strong demand for fixed digital radiography systems, mobile X-ray platforms, C-arm systems, DRF units, and mammography equipment across hospitals, ambulatory surgical centers, and independent diagnostic facilities.

X-ray imaging remains a foundational diagnostic modality within the U.S. healthcare system due to its clinical versatility, cost efficiency, and rapid imaging capabilities. It is widely used in emergency medicine, orthopedics, pulmonology, oncology screening, trauma evaluation, and interventional procedures. The United States X-ray Market benefits from mature healthcare infrastructure, high imaging procedure volumes, and structured reimbursement systems that support ongoing equipment modernization.

The market is characterized by steady replacement cycles, digital system upgrades, and integration of advanced workflow technologies that improve diagnostic efficiency across healthcare networks.

United States X-ray Market Size and Forecast (2024–2031)

The United States X-ray Market demonstrates consistent growth supported by structured hospital procurement cycles and stable imaging demand.

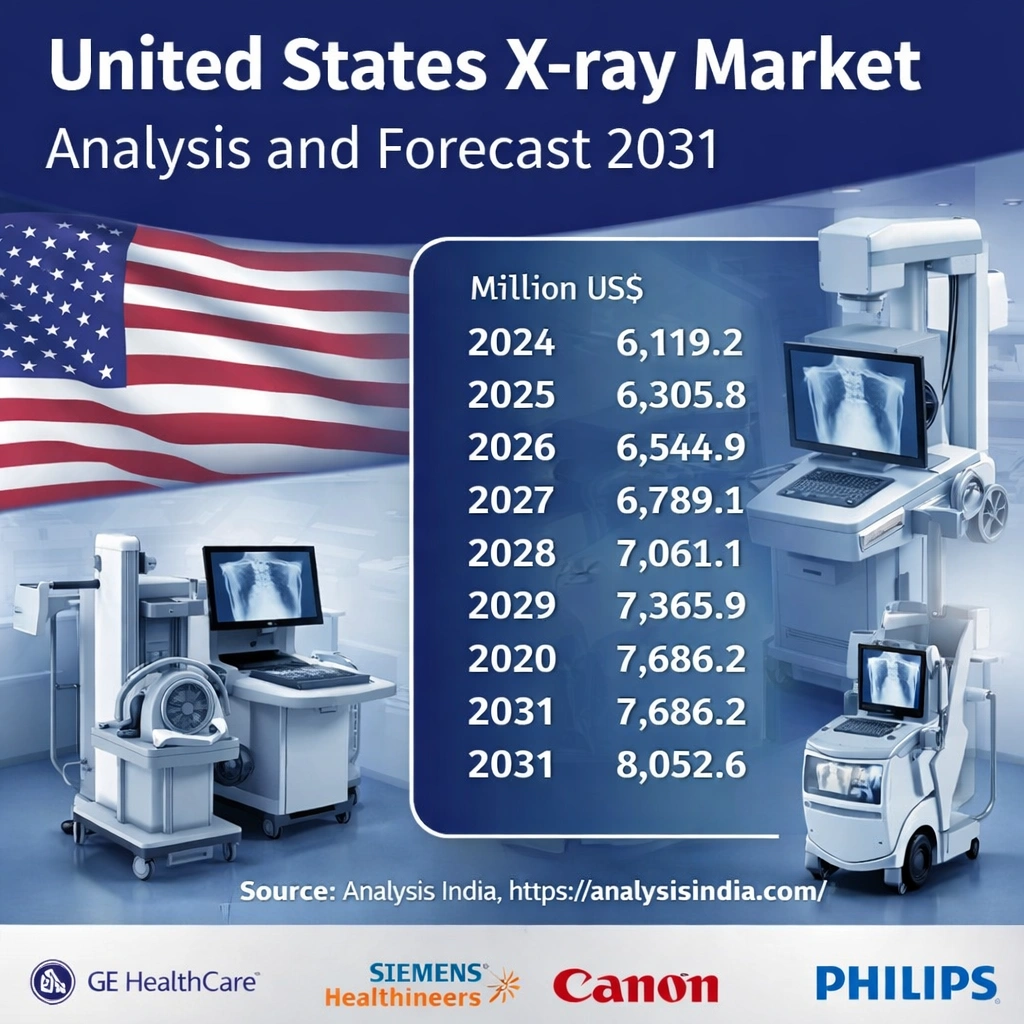

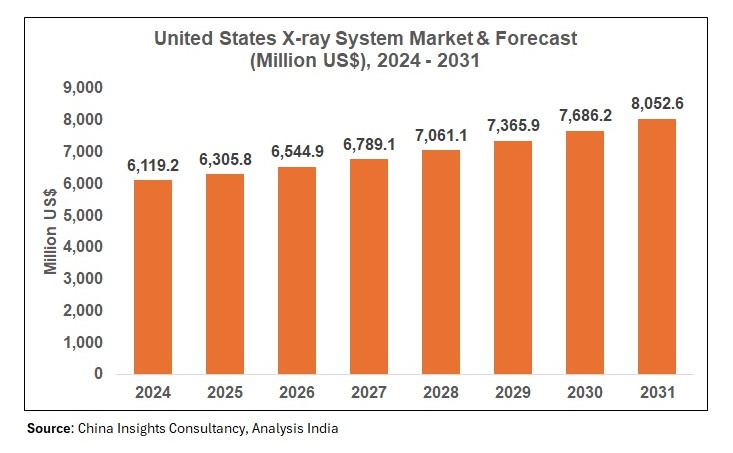

By 2031, the United States X-ray Market is projected to reach US$ 8,052.6 million, reflecting steady expansion driven primarily by system replacement, digital upgrades, and operational efficiency improvements within radiology departments. Growth in the U.S. market is less dependent on new hospital construction and more closely linked to technology modernization and equipment lifecycle renewal.

Healthcare Infrastructure Supporting the United States X-ray Market

The strength of the United States X-ray Market is closely tied to the country’s extensive healthcare infrastructure. The United States maintains a large network of hospitals, outpatient centers, ambulatory surgical facilities, and specialized imaging clinics that collectively generate substantial diagnostic imaging volume.

Urban healthcare systems demonstrate high equipment density and frequent technology upgrades, while rural facilities are gradually modernizing imaging capabilities through public funding initiatives and hospital network consolidation. The expansion of outpatient care models has further increased demand for compact and mobile X-ray systems, particularly in emergency and critical care environments.

This infrastructure depth ensures stable and predictable utilization rates for X-ray systems across clinical specialties.

Regulatory Framework

The United States X-ray Market operates under strict regulatory oversight to ensure patient safety and equipment performance. All X-ray systems must receive clearance from the U.S. Food and Drug Administration before commercial deployment. Regulatory requirements include radiation safety compliance, clinical validation testing, and adherence to manufacturing quality standards.

Reimbursement policies also significantly influence procurement decisions. Imaging procedures are reimbursed under frameworks managed by the Centers for Medicare & Medicaid Services. Medicare and Medicaid policies play a central role in shaping hospital investment strategies, particularly in publicly funded institutions.

Regulatory transparency and reimbursement stability contribute to structured replacement cycles and consistent equipment demand across the United States X-ray Market.

Technology Adoption Trends

The United States X-ray Market demonstrates high penetration of digital radiography systems, with analog systems largely phased out in major healthcare institutions. Hospitals continue to upgrade to advanced flat-panel detector systems that improve image clarity while optimizing radiation dose management.

Artificial intelligence is increasingly integrated into imaging workflows to enhance reporting efficiency and assist radiologists in image prioritization. AI-enabled tools support operational productivity by improving turnaround time and reducing workflow bottlenecks.

Mobile digital radiography systems are experiencing steady adoption, particularly in emergency departments and intensive care units. Their flexibility aligns with decentralized care models and expanding bedside imaging requirements. Integration with PACS and electronic health record systems further strengthens workflow coordination across hospital networks.

Segmentation of the United States X-ray Market

The United States X-ray Market includes a broad range of system categories serving diverse clinical applications. Fixed digital radiography systems represent the largest installed base, primarily within hospital radiology departments where high imaging volumes require stable and high-performance platforms.

Mobile digital radiography systems are increasingly used in acute care settings to support bedside imaging and emergency diagnostics. Mammography systems maintain consistent demand due to structured screening programs and preventive healthcare initiatives. C-arm systems, both fixed and mobile, support surgical and interventional procedures across orthopedic and cardiovascular specialties. DRF systems serve specialized diagnostic environments requiring integrated fluoroscopy and radiography capabilities.

Hospitals remain the largest end-user segment, followed by outpatient imaging centers and ambulatory surgical facilities.

Procurement and Replacement Trends

Procurement activity within the United States X-ray Market is largely driven by structured equipment replacement cycles. Hospitals typically operate on multi-year capital budgeting plans, replacing imaging systems every seven to ten years depending on utilization rates and technological advancements.

Group purchasing organizations negotiate bundled agreements that include equipment acquisition, installation, service contracts, and software upgrades. Long-term maintenance agreements play a significant role in total cost of ownership calculations.

Rather than rapid expansion in facility numbers, growth in the United States X-ray Market is primarily supported by modernization of existing imaging infrastructure and adoption of upgraded digital platforms.

Competitive Landscape

The competitive environment of the United States X-ray Market includes globally recognized manufacturers with strong domestic distribution and service networks. Major industry participants include GE HealthCare, Siemens Healthineers, Canon Medical Systems, and Philips.

Competition is based on detector performance, AI integration capabilities, workflow software, service coverage, and long-term reliability. Manufacturers increasingly focus on delivering integrated digital ecosystems rather than standalone imaging hardware.

Service responsiveness and regional support infrastructure remain critical differentiators within the U.S. market.

Regional Trends

Regional variation exists within the United States X-ray Market. Urban healthcare networks generally demonstrate faster adoption of advanced digital technologies compared to rural facilities, where budget constraints and infrastructure limitations may slow modernization.

Large metropolitan regions exhibit higher equipment replacement frequency due to greater patient throughput and competitive healthcare environments. Meanwhile, rural modernization initiatives continue to improve imaging access in underserved communities.

These regional differences create gradual but stable demand across diverse healthcare settings.

Growth Drivers

The United States X-ray Market is supported by demographic and clinical demand factors. An aging population increases the need for diagnostic imaging related to chronic diseases and degenerative conditions. High emergency department utilization rates further sustain imaging volumes across hospitals.

Preventive screening programs, including mammography initiatives, also contribute to stable demand. Continued digital transformation within radiology departments supports system upgrades and workflow enhancements.

Challenges

Despite steady growth, the United States X-ray Market faces structural challenges. Capital expenditure constraints can delay procurement decisions, particularly in smaller healthcare facilities. Workforce shortages in radiology departments may also affect system utilization rates.

Changes in reimbursement policies and evolving regulatory standards require continuous compliance investment from manufacturers and healthcare providers. Rural healthcare disparities continue to influence uneven technology adoption across regions.

Future Outlook

The outlook for the United States X-ray Market remains stable and innovation-driven through 2031. Continued digital modernization, integration of AI-enabled workflow tools, and structured replacement cycles are expected to sustain revenue expansion.

As healthcare systems prioritize operational efficiency and diagnostic precision, the United States X-ray Market will remain a key regional contributor to the Global X-ray System Market and a leading adopter of advanced imaging technologies.

Conclusion

The United States X-ray Market represents a mature yet evolving diagnostic imaging segment supported by strong healthcare infrastructure, structured reimbursement systems, and continuous technology modernization. With projected revenue reaching US$ 8,052.6 million by 2031, the market reflects stable replacement-driven growth and sustained demand across clinical settings.

Digital transformation, regulatory stability, and integration of advanced imaging solutions will continue shaping the development of the United States X-ray Market in the coming years.

Frequently Asked Questions

What is the projected size of the United States X-ray Market by 2031?

The United States X-ray Market is projected to reach US$ 8,052.6 million by 2031.

What drives growth in the United States X-ray Market?

Growth is driven by system replacement cycles, digital radiography adoption, aging population trends, and stable imaging procedure volumes.

Which system type dominates the United States X-ray Market?

Fixed digital radiography systems dominate due to widespread installation in hospital radiology departments.

How is the United States X-ray Market regulated?

The market is regulated by the U.S. Food and Drug Administration, with reimbursement frameworks influenced by Medicare and Medicaid policies.