Japan Cancer Screening Market Overview

The Japan cancer screening market is emerging as one of the most structured and technologically advanced segments within the global healthcare ecosystem. The country’s healthcare system has long emphasized preventive care, early diagnosis, and systematic screening programs. This strong foundation has enabled Japan to build a mature cancer screening infrastructure that continues to evolve with innovation and demographic pressure.

Japan stands out globally due to its unique combination of aging demographics, universal healthcare coverage, and high healthcare utilization rates. The population aged 65 and above accounts for nearly 30 percent of the total population, making Japan one of the most rapidly aging societies in the world. This demographic shift significantly increases the prevalence of cancer and reinforces the importance of early detection through organized screening systems.

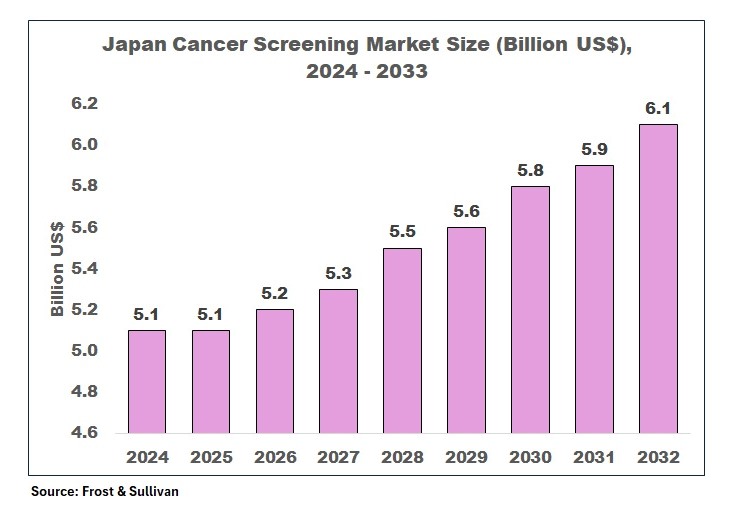

The Japan cancer screening market is projected to grow steadily from USD 5.1 billion in 2024 to USD 6.3 billion by 2033, reflecting consistent expansion rather than volatile growth. This stability is largely driven by government-backed screening programs, rising awareness of preventive healthcare, and continuous technological advancements in diagnostic tools.

For global market context and macro-level insights, refer to the article: Cancer Screening Market Growth Trends Insights

Japan Cancer Screening Market Size Analysis and Forecast

The Japan cancer screening market size reflects a gradual but highly sustainable growth trajectory. Unlike emerging markets that experience rapid spikes, Japan demonstrates a mature growth pattern supported by policy stability, technological adoption, and consistent healthcare spending.

This steady progression indicates that the Japan cancer screening market is driven by long-term structural factors rather than short-term demand fluctuations. The market benefits from continuous government support, increasing participation rates, and the integration of digital healthcare technologies.

Additionally, the broader population screening market in Japan is expected to grow at a CAGR of around 6.5 percent, supported by rising chronic disease incidence and advancements in diagnostic technologies. This further reinforces the growth potential of the Japan cancer screening market as a key subset.

Market Dynamics of Japan Cancer Screening Market

The Japan cancer screening market operates within a complex ecosystem influenced by demographic, technological, economic, and policy-driven factors. A deeper analysis reveals multiple layers of growth drivers and structural challenges.

Aging Population as the Core Growth Engine

One of the most critical factors shaping the Japan cancer screening market is the country’s aging population. With one of the highest life expectancies globally and a declining birth rate, Japan is experiencing a demographic imbalance that directly impacts healthcare demand.

Older populations are significantly more prone to cancers such as colorectal, lung, prostate, and breast cancer. As a result, screening programs are becoming increasingly essential in managing healthcare costs and improving patient outcomes. The aging factor does not just increase demand but also shifts the focus toward frequent and advanced screening methods.

Rising Cancer Burden and Mortality Trends

Although Japan has achieved progress in reducing mortality rates for certain cancers such as stomach and liver cancer, other cancers like colorectal, breast, and cervical cancer continue to pose significant challenges.

This mixed trend highlights the need for more effective and widespread screening programs. The Japan cancer screening market is therefore evolving to address these gaps through enhanced early detection strategies and improved diagnostic accuracy.

Government Policies and Public Health Programs

The Japanese government plays a central role in the Japan cancer screening market through national and municipal screening programs. These programs are designed to detect cancer at early stages and are often subsidized to ensure accessibility.

Cancer screening in Japan is typically divided into two categories:

- Municipal screening programs

- Workplace-based screening programs

These structured approaches ensure broad population coverage, although participation rates still vary across regions and demographics.

Technology Landscape in Japan Cancer Screening Market

The Japan cancer screening market is at the forefront of technological innovation, integrating advanced diagnostic tools that significantly enhance screening accuracy and efficiency.

AI and Digital Diagnostics

Artificial intelligence is transforming the screening landscape by improving image analysis, reducing diagnostic errors, and accelerating detection timelines. AI-powered systems are increasingly being used in radiology, pathology, and genomic analysis.

Liquid Biopsy and Genomic Screening

Emerging technologies such as liquid biopsy and next-generation sequencing are gaining traction in the Japan cancer screening market. These methods enable non-invasive detection of cancer biomarkers, making screening more accessible and less uncomfortable for patients.

Imaging and Diagnostic Equipment

Advanced imaging technologies such as MRI, CT scans, and mammography continue to dominate the market. The demand for high-precision diagnostic equipment is increasing as healthcare providers aim to improve early detection rates.

The growth of Japan’s cancer diagnostics segment, which is expected to expand significantly over the next decade, further supports the expansion of screening technologies.

Japan Cancer Screening Market Segmentation Analysis

The Japan cancer screening market demonstrates a highly structured segmentation framework that reflects the country’s advanced healthcare ecosystem and targeted disease management strategies. Unlike emerging markets where screening adoption is fragmented, Japan’s segmentation is driven by clinical guidelines, government-backed programs, and high awareness levels among the population. This creates a well-defined distribution of screening demand across multiple cancer types, technologies, and healthcare settings.

From a cancer type perspective, the Japan cancer screening market is primarily dominated by screening programs for colorectal, lung, breast, cervical, and prostate cancers. Colorectal cancer screening holds a significant share due to its high incidence rate and strong government emphasis on early detection through fecal occult blood tests and colonoscopy procedures. According to the World Health Organization cancer facts, colorectal and lung cancers remain among the most commonly diagnosed cancers globally, reinforcing the importance of structured screening programs. Similarly, lung cancer screening has gained prominence due to Japan’s historical smoking prevalence, with low-dose CT scans increasingly being adopted for early-stage detection.

Breast cancer screening continues to expand steadily, supported by nationwide mammography programs and awareness campaigns targeting women above 40 years of age. Cervical cancer screening, although well-established, still presents opportunities for growth due to variations in participation rates, particularly among younger demographics. The OECD health statistics database highlights that screening participation rates in developed economies like Japan still have room for improvement, which directly impacts market expansion.

From a technology standpoint, the Japan cancer screening market is evolving beyond traditional imaging methods toward a hybrid model that integrates molecular diagnostics, biomarker-based screening, and genetic testing. Imaging technologies such as MRI, CT scans, and mammography remain foundational, but the increasing adoption of liquid biopsy and genomic screening is transforming the landscape. These advanced technologies enable early detection at a molecular level, often before symptoms appear, which significantly enhances survival rates and reduces treatment costs. Research published on National Center for Biotechnology Information (NCBI) confirms that molecular diagnostics are playing a critical role in improving early cancer detection outcomes.

In terms of end users, hospitals continue to dominate the Japan cancer screening market due to their comprehensive infrastructure, availability of specialized professionals, and integration with national screening programs. Diagnostic laboratories are also playing an increasingly important role, particularly in molecular and genetic testing, as demand for precision diagnostics rises. Research institutes contribute to innovation and technological advancement, ensuring that Japan remains at the forefront of cancer screening development. This multi-layered segmentation highlights the depth and maturity of the Japan cancer screening market, positioning it as a benchmark for structured healthcare delivery.

Market Trends Shaping Japan Cancer Screening Market

The Japan cancer screening market is undergoing a significant transformation driven by evolving healthcare priorities, technological innovation, and changing patient behavior. One of the most prominent trends is the shift toward preventive healthcare. Japan’s healthcare system is increasingly focusing on early detection rather than reactive treatment, which aligns with the country’s demographic challenges and long-term cost management strategies. According to the WHO noncommunicable diseases report, early screening significantly reduces mortality rates, further strengthening the case for preventive healthcare systems.

Another key trend shaping the Japan cancer screening market is the integration of digital health technologies and data analytics. Electronic health records, cloud-based diagnostic platforms, and AI-powered decision support systems are being incorporated into screening workflows. These technologies enable better patient tracking, improved diagnostic accuracy, and more efficient resource allocation. Insights from McKinsey healthcare insights indicate that AI-driven diagnostics can improve detection efficiency significantly, making them a critical component of modern screening systems.

The growing adoption of non-invasive screening methods is also redefining the Japan cancer screening market. Patients are increasingly opting for less invasive procedures such as liquid biopsy and advanced imaging techniques, which offer higher comfort and convenience. This trend is particularly important in improving participation rates, as fear and discomfort have traditionally been barriers to screening. Additionally, the expansion of private diagnostic centers is contributing to increased accessibility and service diversity, further strengthening market growth.

Awareness campaigns and public health initiatives are playing a crucial role in shaping the Japan cancer screening market. Government agencies and healthcare organizations are actively promoting the importance of early detection through education and outreach programs. While these efforts have improved participation rates, there is still room for growth, particularly in rural areas and among younger populations. Overall, these trends indicate a dynamic and evolving market landscape that is well-positioned for sustained growth.

Comparative Analysis with Global Markets

The Japan cancer screening market occupies a unique position in the global landscape, characterized by a balance between technological advancement, government support, and stable growth dynamics. When compared to other major markets, Japan’s approach to cancer screening reflects a combination of efficiency, accessibility, and innovation.

In comparison with the United States Cancer Screening Market the Japanese market is less driven by private sector competition and more influenced by government-led initiatives. The United States benefits from rapid technological innovation and high healthcare spending, but it also faces challenges related to cost variability and unequal access. According to the Centers for Medicare & Medicaid Services (CMS), healthcare expenditure in the US is significantly higher, which directly impacts screening affordability.

When compared to the China Cancer Screening Market Japan demonstrates a higher level of technological maturity and healthcare infrastructure development. China’s market is expanding rapidly due to its large population and increasing healthcare investments, but it still faces challenges related to regional disparities and limited access in rural areas. Reports from the World Bank healthcare data highlight disparities in healthcare access across developing regions, which contrasts with Japan’s more uniform system.

These comparisons highlight the strengths of the Japan cancer screening market, particularly its stability, technological sophistication, and strong policy framework.

Challenges in Japan Cancer Screening Market

Despite its advanced infrastructure and strong policy support, the Japan cancer screening market faces several challenges that could impact its long-term growth and efficiency. One of the primary challenges is the allocation of financial resources. Cancer screening programs require significant investment in equipment, personnel, and outreach initiatives. According to research available on PubMed Central, budget limitations at local government levels can restrict screening expansion and reduce participation rates.

Another major challenge is the relatively low participation rate in certain screening programs. While Japan has established comprehensive screening systems, actual participation varies across regions and demographics. Studies referenced in BMJ Evidence-Based Medicine indicate that participation rates for some cancer screenings remain below optimal levels, highlighting a gap between availability and utilization.

Workforce shortages also pose a significant challenge. Japan is experiencing a decline in its working-age population, which affects the availability of healthcare professionals. This shortage is particularly evident in rural areas, where access to specialized diagnostic services may be limited.

Additionally, the risk of overdiagnosis is becoming an increasingly important concern in the Japan cancer screening market. Advanced screening technologies can detect abnormalities that may not progress into serious conditions, leading to unnecessary treatments and increased healthcare costs.

Opportunities in Japan Cancer Screening Market

The Japan cancer screening market offers numerous opportunities for growth, innovation, and strategic development. One of the most significant opportunities lies in the expansion of artificial intelligence and automation. AI-driven diagnostic tools have the potential to improve accuracy, reduce workload, and enhance efficiency, making screening programs more scalable and cost-effective. According to

World Economic Forum healthcare insights, AI is expected to play a transformative role in global healthcare systems.

The rise of personalized medicine is another key opportunity. Advances in genomics and molecular diagnostics are enabling more targeted screening approaches, allowing healthcare providers to identify high-risk individuals and tailor screening strategies accordingly. This shift toward precision healthcare is expected to drive significant growth in the Japan cancer screening market.

Investment in healthcare infrastructure and digital transformation is also creating new opportunities. The integration of telemedicine, remote diagnostics, and digital health platforms can improve access to screening services, particularly in underserved areas.

Furthermore, increasing collaboration between public and private sectors is expected to enhance the efficiency and reach of screening programs. Partnerships between government agencies, healthcare providers, and technology companies can accelerate innovation and improve service delivery.

Future Outlook of Japan Cancer Screening Market

The future of the Japan cancer screening market is characterized by steady growth, technological advancement, and a strong emphasis on preventive healthcare. As the country continues to address its demographic challenges, the importance of early detection and efficient screening systems will become even more pronounced.

The market is expected to reach USD 6.3 billion by 2033, driven by continuous innovation, policy support, and increasing awareness of the benefits of early detection. The integration of advanced technologies such as AI, liquid biopsy, and genomic screening will further enhance the effectiveness and accessibility of screening programs.

In addition, the focus on digital health and data-driven decision-making is expected to transform the Japan cancer screening market. According to Deloitte healthcare outlook, digital transformation is a key driver of efficiency and innovation in modern healthcare systems.

Conclusion

The Japan cancer screening market represents a mature and highly organized segment within the global healthcare industry. Its growth is driven by a unique combination of demographic trends, technological advancements, and strong government support.

While challenges such as funding constraints, participation gaps, and workforce shortages persist, the overall outlook remains positive. The continued focus on innovation, preventive healthcare, and digital transformation will play a crucial role in shaping the future of the Japan cancer screening market.

As Japan continues to refine its screening strategies and adopt new technologies, it sets a global benchmark for efficient and effective cancer detection systems. The Japan cancer screening market will not only contribute to improved patient outcomes but also serve as a model for other countries seeking to enhance their healthcare infrastructure and reduce the burden of cancer.

FAQ – Japan Cancer Screening Market

What is the Japan cancer screening market size in 2033

The Japan cancer screening market is expected to reach around USD 6.3 billion by 2033, driven by aging population and advanced diagnostic technologies.

What is driving the Japan cancer screening market growth

The Japan cancer screening market is growing due to increasing cancer cases, strong government screening programs, and rising adoption of AI and non invasive diagnostic tools.

Which cancers are commonly screened in Japan

The Japan cancer screening market mainly focuses on colorectal, lung, breast, cervical, and prostate cancers due to their high prevalence.

How does Japan support cancer screening programs

The Japanese government supports the Japan cancer screening market through national and municipal screening programs that promote early detection and preventive healthcare.

What are the latest trends in Japan cancer screening market

Key trends in the Japan cancer screening market include AI based diagnostics, liquid biopsy, digital health integration, and increasing use of non invasive screening methods.