📅 Published: April 23, 2026

🔄 Last Updated: April 23, 2026

United States Lung Cancer Molecular Screening Market Overview

The United States Lung Cancer Molecular Screening Market is emerging as a critical component of modern oncology diagnostics, driven by the growing need for early detection, precision medicine, and improved patient outcomes. Molecular screening is transforming how lung cancer risk is identified by focusing on biomarkers, genetic mutations, and biological signals rather than relying only on imaging-based techniques.

This shift is strongly connected with the broader expansion of the United States Lung Cancer Screening Market, where traditional screening methods such as low-dose CT scans continue to play an important role. However, molecular screening enhances these methods by providing deeper biological insights, helping clinicians identify high-risk patients earlier and more accurately.

The increasing adoption of molecular diagnostics also aligns with trends highlighted in the Lung Cancer Molecular Screening Market Growth, where biomarker-based technologies are reshaping early detection strategies. As healthcare systems across the United States continue to emphasize preventive care and personalized treatment, the United States Lung Cancer Molecular Screening Market is expected to expand steadily.

United States Lung Cancer Molecular Screening Market Size and Forecast

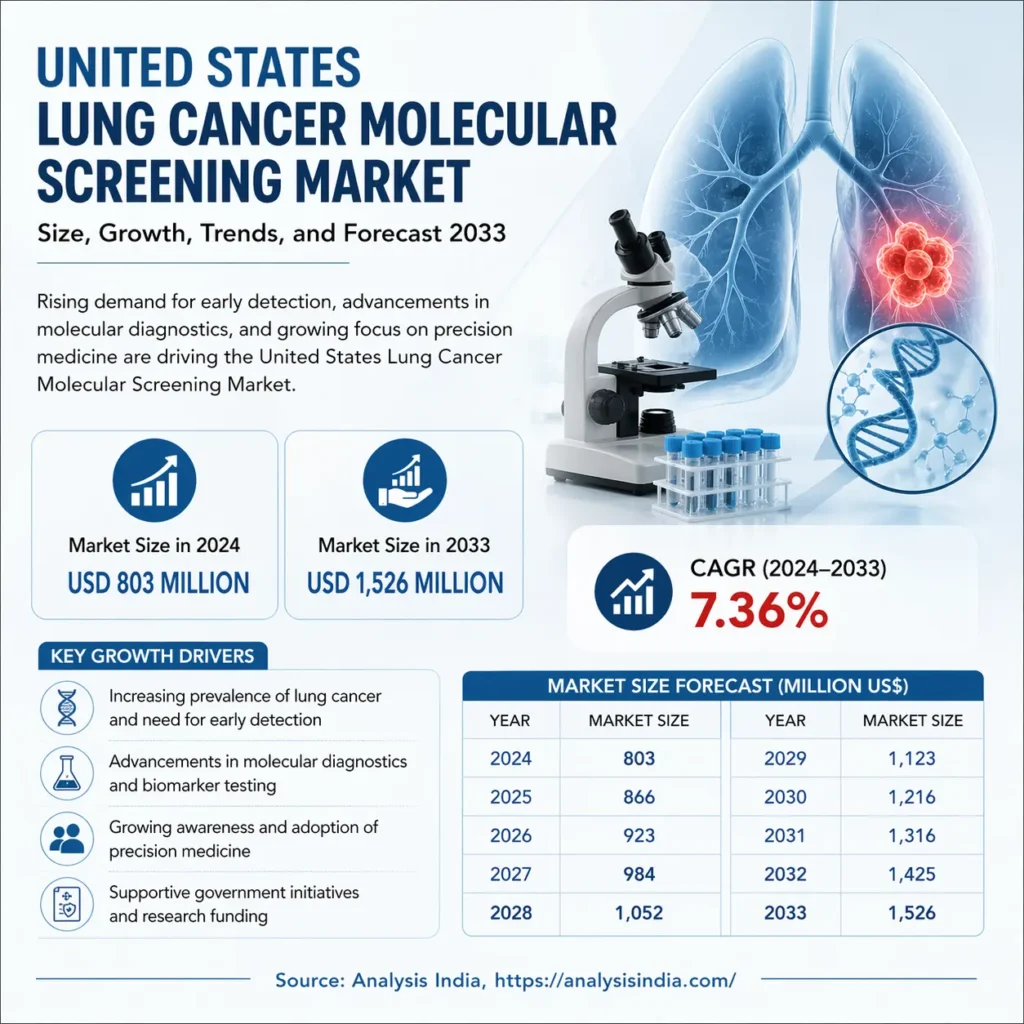

The United States Lung Cancer Molecular Screening Market is valued at USD 803 Million in 2024 and is projected to reach USD 1,526 Million by 2033, expanding steadily over the forecast period. The market is expected to rise from USD 866 Million in 2025 to USD 923 Million in 2026, and then continue its upward path through the end of the decade. This growth pattern reflects a market that is still evolving but already showing strong commercial and clinical momentum. The increasing need for earlier detection and more personalized oncology workflows is expected to support sustained investment in molecular screening technologies across the United States.

United States Lung Cancer Molecular Screening Market Forecast (Million US$)

| Year | Market Size |

|---|---|

| 2024 | 803 |

| 2025 | 866 |

| 2026 | 923 |

| 2027 | 984 |

| 2028 | 1,052 |

| 2029 | 1,123 |

| 2030 | 1,216 |

| 2031 | 1,316 |

| 2032 | 1,425 |

| 2033 | 1,526 |

Source: Frost & Sullivan

The forecast shows a steady year-on-year increase that reflects a healthy and sustained expansion in the United States Lung Cancer Molecular Screening Market. Growth in this segment is being supported by stronger adoption of molecular diagnostics in cancer care pathways, broader awareness among clinicians, and the rising importance of risk-based screening approaches. The market also benefits from the fact that molecular screening is not a one-time innovation. Instead, it continues to evolve through better assays, improved sensitivity, stronger clinical validation, and expanding use cases in real-world oncology settings.

The step-up from USD 803 Million in 2024 to USD 1,526 Million in 2033 also suggests that the market is gaining long-term acceptance, not just short-term interest. As clinical evidence improves and reimbursement discussions continue to mature, more providers are likely to explore molecular screening as part of a broader lung cancer detection strategy. This gives the market a strong foundation for long-range growth and positions it as a valuable cluster topic within the wider oncology diagnostics space. This trend is also supported by broader developments discussed in the Lung Cancer Screening Market Growth, where early detection is becoming a central focus of oncology care.

Key Growth Drivers of the United States Lung Cancer Molecular Screening Market

Rising demand for early detection

Early detection remains one of the strongest underlying forces supporting the United States Lung Cancer Molecular Screening Market. Lung cancer is often diagnosed at a later stage, which can make treatment more complex and outcomes less favorable. Molecular screening is drawing attention because it may help identify biological signals earlier in the disease journey. This is particularly important in a healthcare environment that increasingly values preventive care, risk-based intervention, and cost-aware oncology management. This shift toward preventive care is also reflected in the Cancer Screening Market Growth Trends & Insights, where early-stage detection is gaining strong momentum.

The demand for early detection is not limited to hospitals alone. Diagnostic laboratories, outpatient oncology centers, and academic research institutions are all contributing to the push toward better screening methods. Molecular screening fits this environment because it can complement existing protocols and potentially help clinicians refine who should undergo additional diagnostic follow-up. That utility makes it a strong fit for modern lung cancer management programs..

Expansion of precision medicine

Precision medicine continues to transform the United States Lung Cancer Molecular Screening Market. As clinicians become more familiar with biomarkers, genomic alterations, and test-based decision support, molecular screening is increasingly viewed as a logical and necessary tool in oncology. This shift is encouraging diagnostic firms to invest in new assays and broader clinical validation.

Precision medicine also encourages more collaboration between pharmaceutical companies, diagnostic developers, and research organizations. The result is a more connected ecosystem in which screening, diagnosis, and treatment development can evolve together. In practice, this creates more opportunities for the molecular screening segment to move beyond isolated testing and become part of an integrated care pathway.

Growth in liquid biopsy and non-invasive testing

Non-invasive testing is a major theme in the United States Lung Cancer Molecular Screening Market. Liquid biopsy and related molecular methods are gaining interest because they can offer a more patient-friendly way to evaluate disease risk. These technologies are attractive in a market like the United States, where clinicians and patients often prefer solutions that reduce procedural burden while improving diagnostic insight.

Liquid biopsy approaches are especially appealing because they may provide access to circulating biomarkers that are useful for screening, monitoring, and broader oncology assessment. While these methods do not replace all other forms of lung cancer detection, they strengthen the case for molecular screening as a complementary strategy. The continued maturation of such technologies is expected to support market expansion over the forecast period.

Increasing adoption across large healthcare networks

Large healthcare systems and integrated delivery networks play a major role in shaping the United States Lung Cancer Molecular Screening Market. These organizations often have the clinical volume, technological resources, and institutional structure needed to adopt advanced screening tools. When a new test demonstrates clinical utility and operational efficiency, large networks can accelerate adoption by embedding it into standardized patient care pathways.

This matters because the spread of molecular screening often depends on institutional decision-making rather than individual clinician interest alone. Procurement committees, laboratory directors, oncology program leaders, and care coordination teams all influence adoption. As more healthcare systems look for better ways to manage high-risk lung cancer populations, the market gains additional support.

Why the United States Lung Cancer Molecular Screening Market Is Expanding

The growth of the United States Lung Cancer Molecular Screening Market is being shaped by a combination of medical, technological, and commercial factors. One of the strongest drivers is the clinical need to identify lung cancer at an earlier stage, when treatment options are often more effective and patient outcomes can improve. Molecular screening offers a more targeted approach by examining biomarkers and genetic patterns that may indicate the presence of disease risk before symptoms become more visible. This is a major shift from reactive diagnosis toward proactive disease detection.

Another important reason for expansion is the growing role of precision oncology. Healthcare providers in the United States are increasingly comfortable using molecular data to guide screening and diagnostic decisions. This aligns well with the broader trend toward personalized medicine, where care is adapted to the biology of the patient rather than using a one-size-fits-all approach. In the United States Lung Cancer Molecular Screening Market, that trend is creating a strong rationale for the adoption of advanced molecular assays, companion testing tools, and laboratory-developed screening solutions.

The market is also expanding because of improved awareness among both clinicians and patients. Lung cancer screening has become a more visible topic in preventive oncology, especially for populations considered at higher risk. As awareness rises, so does interest in new screening methods that can potentially offer more reliable or more actionable clinical insights. Molecular screening is attractive because it can support earlier intervention, strengthen patient stratification, and complement standard imaging-based screening pathways.

Technology improvements are another clear growth factor. Diagnostic companies continue to refine molecular platforms to improve sensitivity, specificity, turnaround time, and scalability. This is important in the United States, where healthcare buyers often expect both clinical performance and operational efficiency. A screening technology must not only be scientifically credible but also practical for hospital laboratories, reference labs, and large health networks. As a result, companies that can combine clinical value with workflow convenience are well positioned in the United States Lung Cancer Molecular Screening Market.

Challenges in the United States Lung Cancer Molecular Screening Market

High testing and implementation costs

Despite the positive outlook, the United States Lung Cancer Molecular Screening Market faces real cost-related challenges. Molecular testing often requires advanced instruments, specialized reagents, technical expertise, and quality control systems. These elements can create a higher financial barrier for smaller laboratories or healthcare providers with limited budgets. Even in larger systems, adoption decisions may be slowed by the need to demonstrate a clear return on investment.

Cost is not only about the test itself. It also includes training, workflow integration, data interpretation, and follow-up coordination. For molecular screening to deliver value, it must fit into clinical operations in a way that is both affordable and sustainable. That means pricing strategy remains one of the most important considerations for vendors operating in this market.

Reimbursement complexity

Reimbursement continues to influence the speed of adoption in the United States Lung Cancer Molecular Screening Market. When coverage pathways are unclear or vary across payer types, providers may hesitate to adopt new molecular screening tools at scale. In oncology diagnostics, reimbursement often plays a decisive role because even clinically promising tests can face slow uptake without a strong payment framework.

This challenge is particularly relevant for newer assays and emerging screening models that may not yet have broad payer recognition. Diagnostic firms must therefore invest in evidence generation, clinical validation, and payer engagement. Without that support, some promising molecular screening solutions may remain limited to pilot programs or select institutions.

Clinical validation requirements

Another challenge is the need for robust clinical validation. The United States Lung Cancer Molecular Screening Market depends heavily on evidence that screening tools actually improve decision-making and patient outcomes. Unlike general laboratory tests, screening methods in oncology must demonstrate not only analytical accuracy but also clinical relevance and practical utility.

This makes validation a long and sometimes expensive process. Companies need to build trust among clinicians, regulators, and payers, which often requires large datasets, multi-site studies, and real-world evidence. As a result, market entry can be demanding, especially for smaller innovators.

Workflow integration and data interpretation

Molecular screening is not just about producing a result. It is also about making that result meaningful in a complex clinical setting. In the United States Lung Cancer Molecular Screening Market, providers need tests that can be integrated into existing oncology workflows without creating delays or confusion. Data interpretation can become challenging when test outputs are highly technical or require specialist review.

Healthcare systems are increasingly looking for streamlined solutions that are easy to order, easy to interpret, and easy to act upon. This means vendors must think beyond the assay itself and address the full workflow experience. Companies that can simplify implementation may gain a competitive advantage over those offering more complex but less practical solutions.

Technology Trends Shaping the Market

Multi-marker and panel-based testing

One of the most visible technology trends in the United States Lung Cancer Molecular Screening Market is the movement toward multi-marker and panel-based testing. Rather than relying on a single biological indicator, many modern screening approaches examine multiple biomarkers to improve performance and widen clinical insight. This can help provide a more robust screening framework, especially in a disease area where early signals may be subtle.

Panel-based testing is attractive because it may improve the likelihood of identifying relevant disease markers while also supporting greater clinical nuance. For the market, this means diagnostic developers are competing not just on sensitivity, but on how well their platforms capture actionable biological information. The ability to offer a broader view of risk is becoming an important differentiator.

Integration with digital pathology and AI-enabled interpretation

Digital pathology and AI-enabled interpretation are beginning to influence the United States Lung Cancer Molecular Screening Market. While molecular screening is fundamentally a biological process, the surrounding ecosystem increasingly depends on digital tools for interpretation, reporting, and patient stratification. Artificial intelligence can support the analysis of complex datasets and help clinicians identify patterns that might be difficult to assess manually.

This trend is still evolving, but it is important because it shows how the market is moving toward smarter and more connected diagnostic workflows. As healthcare organizations seek better efficiency and consistency, digital support tools may become a natural companion to molecular screening platforms. Over time, this could improve the scalability and usability of screening programs.

Stronger focus on minimally invasive workflows

Minimally invasive workflows are becoming increasingly important in the United States Lung Cancer Molecular Screening Market. Patients and providers both value solutions that reduce discomfort, shorten turnaround times, and simplify follow-up. This preference supports the expansion of molecular methods that can work with blood-based or other low-burden samples.

The appeal of minimally invasive testing is especially high in preventive care settings. A screening approach that is less intimidating and easier to repeat may improve patient participation and support more consistent clinical monitoring. That is one reason why molecular screening has gained such strong interest in the United States.

United States Lung Cancer Molecular Screening Market Segmentation Insights

The United States Lung Cancer Molecular Screening Market can be understood through several important segmentation lenses. Although this article is not structured as a formal product taxonomy report, it is useful to consider how market demand typically breaks down across test type, sample type, end user, and technology platform. These dimensions help explain where adoption is strongest and where future growth may emerge.

By test type

The market includes different screening test formats, ranging from genomic-based assays to biomarker panels and other molecular approaches. Genomic testing often attracts attention because of its ability to identify relevant alterations with high precision. Biomarker panels are also important because they allow for a broader screening view that can be aligned with lung cancer risk assessment. In the United States Lung Cancer Molecular Screening Market, test type matters because different care settings may require different levels of complexity and clinical depth.

By sample type

Sample type is another major factor. Blood-based screening methods are drawing attention because they are easier to collect, less invasive, and often more convenient for repeat testing. Tissue-based approaches may still be relevant in certain clinical situations, but the broader market trend favors approaches that can reduce procedural burden. This makes sample flexibility a meaningful competitive advantage for vendors.

By end user

The primary end users in the United States Lung Cancer Molecular Screening Market include hospitals, diagnostic laboratories, cancer research centers, and specialty clinics. Hospitals remain central because they manage high volumes of complex patients and often lead early adoption. Diagnostic laboratories contribute through test processing and scale. Research centers support evidence generation, while specialty clinics help extend screening access to targeted patient groups.

By technology platform

Technology platforms in this market may include PCR-based systems, sequencing-based systems, and other molecular methods. Each platform offers different advantages in terms of accuracy, throughput, and cost. The right choice often depends on the clinical objective and the resources of the provider. As the market evolves, platforms that combine strong performance with practical workflow integration will be best positioned.

Competitive Landscape of the United States Lung Cancer Molecular Screening Market

The competitive environment in the United States Lung Cancer Molecular Screening Market is shaped by a mix of established diagnostic companies, emerging biotech firms, and research-driven developers. Competition is not simply about launching a test. It is about proving that the test has meaningful clinical utility, fits into real healthcare workflows, and can be supported through payer and provider relationships. This means the market tends to reward companies that can pair scientific credibility with commercial execution.

Large diagnostics players often benefit from distribution strength, brand recognition, and existing laboratory infrastructure. These advantages help them scale faster once a product gains traction. At the same time, smaller innovators can compete effectively by focusing on novel biomarker approaches, improved sensitivity, or specialized screening methods for high-risk populations. The market is therefore competitive but also open to differentiated innovation.

Strategic partnerships are likely to remain important. In many cases, diagnostic developers collaborate with hospital systems, research institutions, or oncology networks to validate technology and expand reach. These partnerships help reduce adoption barriers by building clinical trust and demonstrating utility in real-world settings. For the United States Lung Cancer Molecular Screening Market, that collaborative model is often the shortest path from innovation to implementation.

Commercial competition also extends to service quality. Turnaround time, reporting clarity, support services, and ease of ordering all matter in a screening market. Providers do not just compare analytical performance. They compare the full experience. Vendors that can simplify the clinical workflow while maintaining strong scientific performance are likely to be favored.

Regional and Institutional Demand Patterns

Demand in the United States Lung Cancer Molecular Screening Market is shaped by the distribution of advanced healthcare infrastructure across the country. Major metropolitan areas, academic medical centers, and large integrated health systems usually show faster adoption because they have more resources and stronger exposure to advanced oncology practices. These institutions are often early adopters of emerging molecular technologies and play a key role in setting clinical precedent.

At the same time, regional variation can be significant. States and healthcare markets with stronger cancer center networks may adopt molecular screening earlier than regions with fewer specialized oncology resources. This creates a layered market structure where innovation often begins in high-capability institutions and gradually spreads outward as evidence, reimbursement, and awareness improve.

Institutional demand is also influenced by patient demographics and lung cancer risk profiles. Areas with higher smoking prevalence, older populations, or stronger oncology referral systems may have more immediate need for screening tools. That said, the long-term opportunity lies in broader integration across the United States, especially if molecular screening becomes more standardized in preventive oncology pathways.

Role of Clinical Awareness and Patient Education

The future of the United States Lung Cancer Molecular Screening Market depends not only on technology but also on awareness. Many screening innovations do not scale quickly unless clinicians understand how to use them and patients understand why they matter. For lung cancer molecular screening, patient education is especially important because screening decisions often involve risk perception, eligibility questions, and follow-up planning.

Clinician education helps ensure that molecular results are interpreted correctly and used appropriately in the broader diagnostic pathway. This is essential in a field where overuse, underuse, or misinterpretation can reduce value. Providers need clear clinical frameworks that explain when molecular screening is useful, how it should be combined with other methods, and what actions should follow a positive or inconclusive result.

Patient education plays a different but equally important role. Patients who understand the purpose of screening are more likely to engage in preventive care and follow through with recommended testing. In the United States Lung Cancer Molecular Screening Market, educational outreach can therefore improve adoption while also strengthening trust in newer diagnostic tools.

Investment and Innovation Outlook

The investment environment for the United States Lung Cancer Molecular Screening Market remains attractive because the segment sits at the intersection of oncology, diagnostics, and precision medicine. Investors and strategic buyers are often drawn to markets with strong clinical need, recurring testing potential, and room for technological differentiation. Lung cancer molecular screening meets all three conditions.

Innovation in this market may focus on better biomarker identification, more efficient sample processing, broader clinical utility, and enhanced integration with digital health systems. Companies that can reduce cost while improving performance are likely to stand out. In addition, innovations that help connect screening results to treatment pathways may be especially valuable because they strengthen the broader care continuum.

A large part of the market’s long-term appeal comes from its scalability. As more evidence becomes available and adoption barriers decrease, molecular screening can expand across more providers and patient groups. That creates an environment where growth is not tied to one single product cycle but to a larger transformation in how lung cancer risk is assessed and managed.

Strategic Opportunities for Market Participants

There are several strategic opportunities in the United States Lung Cancer Molecular Screening Market for companies that want to build a strong position. One opportunity is to focus on clinical utility and evidence generation. Markets like this reward credible data, especially when tests are intended for early detection or risk stratification. Another opportunity is to develop cost-efficient solutions that fit the operational realities of hospitals and laboratories.

Companies can also strengthen their market position by building educational support for clinicians and lab professionals. A test that is easy to understand and easy to use often has a better chance of adoption than one that requires heavy interpretation support. Clear reporting, workflow integration, and strong customer service can all create measurable competitive advantage.

Partnerships are another important route to growth. Collaborations with cancer centers, reference laboratories, and research institutions can help accelerate validation and adoption. In the United States Lung Cancer Molecular Screening Market, these partnerships are not just helpful. They are often essential for scaling trust and credibility.

Increasing Importance of Awareness and Preventive Healthcare

Awareness and education are essential for the continued growth of the United States Lung Cancer Molecular Screening Market. Patients are becoming more proactive about their health, leading to increased demand for early screening options.

According to the National Cancer Institute, early detection significantly improves cancer outcomes, reinforcing the importance of advanced screening methods. Similarly, the Centers for Disease Control and Prevention highlights the role of screening in reducing lung cancer mortality.

The American Cancer Society also emphasizes awareness and early diagnosis as key factors in improving survival rates. These authoritative insights support the growing adoption of molecular screening technologies.

Future Outlook of the United States Lung Cancer Molecular Screening Market

The long-term outlook for the United States Lung Cancer Molecular Screening Market is positive, supported by a steady rise in market value from USD 803 Million in 2024 to USD 1,526 Million in 2033. This growth path suggests that molecular screening will continue to gain relevance as healthcare systems place greater emphasis on early detection, precision oncology, and less invasive diagnostic methods. The market is still developing, but its direction is clear: it is moving toward wider clinical acceptance and stronger integration into routine cancer care.

By 2033, the market is likely to look more mature, with better validated assays, improved workflow integration, and stronger payer and provider familiarity. Adoption may extend more broadly beyond major academic centers as evidence improves and operational barriers fall. The combination of scientific innovation and clinical need makes this one of the more promising areas within oncology diagnostics.

The market is also likely to benefit from the continued shift toward personalized healthcare. As more providers seek tools that can improve patient selection, refine risk assessment, and support early intervention, molecular screening will remain highly relevant. In the United States Lung Cancer Molecular Screening Market, the next decade is likely to be defined by stronger clinical confidence, better access, and broader institutional adoption.

Conclusion

The United States Lung Cancer Molecular Screening Market is positioned for consistent growth over the forecast period, driven by the need for earlier detection, the rise of precision medicine, and the increasing clinical value of molecular diagnostics. With the market expected to grow from USD 803 Million in 2024 to USD 1,526 Million by 2033, it represents a meaningful opportunity for diagnostic companies, healthcare providers, and research organizations focused on oncology innovation. While challenges such as cost, reimbursement, and validation remain important, the long-term outlook is still strong because the market addresses a fundamental clinical need.

FAQs: United States Lung Cancer Molecular Screening Market

What is the United States Lung Cancer Molecular Screening Market?

The United States Lung Cancer Molecular Screening Market refers to the use of advanced molecular tests to detect lung cancer risk at an early stage using biomarkers and genetic data.

What is the market size of the United States Lung Cancer Molecular Screening Market?

The United States Lung Cancer Molecular Screening Market was valued at USD 803 Million in 2024 and is projected to reach USD 1,526 Million by 2033.

What is driving the growth of the United States Lung Cancer Molecular Screening Market?

Growth is driven by early detection demand, rising use of precision medicine, increasing awareness, and advancements in molecular diagnostic technologies.

Why is molecular screening important for lung cancer?

Molecular screening helps identify cancer risk earlier by analyzing biological markers, which supports timely diagnosis and better treatment planning.

Who are the key users of molecular screening in the United States?

Hospitals, diagnostic laboratories, cancer centers, and research institutions are the main users in the United States Lung Cancer Molecular Screening Market.

What are the major challenges in this market?

High testing costs, reimbursement issues, and the need for strong clinical validation are key challenges in the United States Lung Cancer Molecular Screening Market.