📅 Published: April 14, 2026

🔄 Last Updated: April 14, 2026

Analysis India: The China Gastric Cancer Screening Market is one of the most significant and rapidly evolving segments within the global cancer diagnostics landscape. China has one of the highest incidences of gastric cancer globally, making screening programs a national healthcare priority. As a result, the country has developed structured and large-scale screening initiatives that are driving substantial market growth.

The increasing burden of gastric cancer, combined with rising healthcare investments and technological advancements, is fueling expansion in the China Gastric Cancer Screening Market. Government-backed screening programs, along with innovations in diagnostic technologies, are enabling early detection and improving patient outcomes.

Key takeaways:

Strong growth trajectory: Compound growth through 2033 driven by scale‑up of screening programs and commercialization of liquid biopsy and biomarker tests.

Technology shift: Non‑invasive tests (blood‑based biomarkers, multi‑omics panels) will complement and, in some screening contexts, partially substitute endoscopy.

Policy and reimbursement: NMPA approvals and provincial pilot programs are the immediate catalysts for market expansion.

Commercial opportunity: Diagnostics manufacturers, hospital networks, and payers can capture value by aligning test performance, cost, and implementation pathways.

For a broader perspective, refer to the global gastric cancer screening market.

China Gastric Cancer Screening – Market Size and Forecast

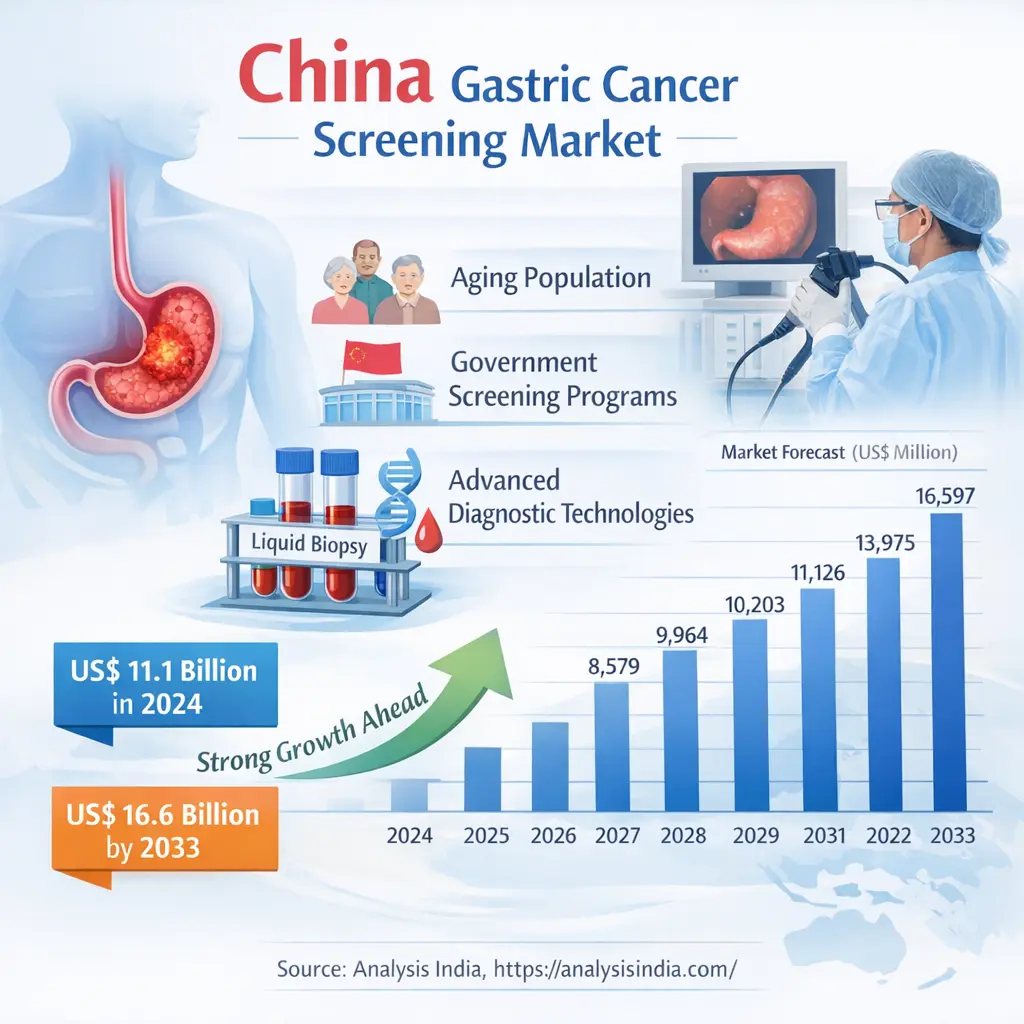

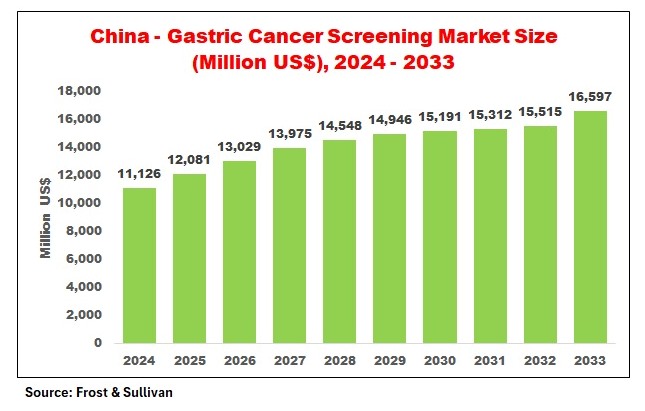

The China Gastric Cancer Screening Market demonstrates a strong upward trajectory, reflecting increasing screening penetration and government support. The consistent growth pattern highlights sustained demand rather than short-term fluctuations.

The China Gastric Cancer Screening Market is entering a phase of accelerated growth driven by a confluence of demographic need, public health policy, and rapid technological innovation. From an estimated US$ 11,126 million in 2024, the market is forecast to reach US$ 16,597 million by 2033, reflecting sustained investment in early detection, broader adoption of non‑invasive diagnostics, and expanding private‑sector participation.

China Gastric Cancer Screening Market is driven by a mix of provincial pilots, hospital networks, and private wellness programs that combine serological panels, breath tests, and ctDNA assays into practical screening pathways. For a deeper examination of liquid biopsy commercialization and regional rollout strategies, read the China liquid biopsy cancer screening market, then compare deployment models in the Japan liquid biopsy cancer screening market and the South East Asia liquid biopsy cancer screening market to identify partnership and distribution approaches that have proven effective.

China Gastric Cancer Screening Market -Market Dynamics

Demand Drivers

1. High disease burden and screening need

China carries a substantial share of global gastric cancer incidence. Population aging, persistent Helicobacter pylori prevalence in some regions, and dietary risk factors sustain a large at‑risk cohort. Public health authorities and hospital systems are prioritizing early detection to reduce mortality and treatment costs, creating a large addressable market for screening solutions.

2. Government programs and provincial pilots National and provincial screening initiatives—often launched as pilot programs in high‑incidence provinces—are expanding. These programs fund population screening, subsidize diagnostic tests, and create procurement pathways for approved technologies. The resulting demand for scalable, cost‑effective screening modalities is a major growth engine.

3. Shift to non‑invasive screening Endoscopy remains the clinical gold standard for diagnosis, but it is resource‑intensive and limited by capacity constraints. Non‑invasive tests—serological biomarker panels, breath tests, and liquid biopsy assays—enable broader population coverage and repeated screening cycles, improving early detection rates and lowering per‑screen costs.

4. Private sector and payer engagement Commercial screening packages offered by private hospitals and health management companies are expanding. Employers and private insurers increasingly cover screening as part of wellness programs, creating parallel demand channels beyond public procurement.

Market Restraints

1. Endoscopy capacity and clinical inertia Despite technological advances, many clinicians and institutions still rely on endoscopy for definitive diagnosis. Integrating new screening tests into clinical pathways requires evidence of clinical utility, cost‑effectiveness, and clear referral algorithms.

2. Reimbursement uncertainty Reimbursement pathways for novel diagnostics remain uneven across provinces. Without consistent reimbursement, adoption in lower‑resource regions will lag.

3. Quality and standardization Variability in test performance, laboratory standards, and reporting can undermine clinician confidence. National guidelines and standardized quality frameworks are needed to scale adoption.

Opportunities

1. Hybrid screening models Combining non‑invasive triage tests with targeted endoscopy for positives can optimize resource use and improve detection rates. This hybrid approach is attractive for large‑scale population programs.

2. Digital health integration AI‑assisted risk stratification, tele‑endoscopy, and centralized lab reporting can accelerate scale and improve follow‑up adherence.

3. Export potential Chinese diagnostic manufacturers that validate performance domestically can pursue regional markets in East and Southeast Asia where gastric cancer incidence is also high.

China Gastric Cancer Screening Market -Technology Landscape

Endoscopy and Imaging

Endoscopy remains the diagnostic anchor for gastric cancer. Advances in endoscopic imaging—high‑definition scopes, narrow‑band imaging, and AI‑assisted lesion detection—improve sensitivity and reduce missed lesions. However, endoscopy’s capital and personnel requirements limit its use as a primary population screening tool.

Role in screening: confirmatory diagnosis and therapeutic intervention (e.g., endoscopic mucosal resection) for screen‑positive individuals.

Serological Biomarkers and Multi‑Analyte Panels

Serological tests measuring pepsinogens, gastrin‑17, H. pylori antibodies, and other biomarkers have been used for risk stratification. Newer multi‑analyte panels combine protein markers, methylation signatures, and microRNA profiles to improve sensitivity and specificity for early‑stage disease.

Advantages: low cost, ease of sample collection, suitability for large‑scale screening.

Limitations: variable sensitivity for early lesions; need for robust validation in Chinese cohorts.

Liquid Biopsy and Circulating Biomarkers

Liquid biopsy—detection of circulating tumor DNA (ctDNA), methylation patterns, and circulating tumor cells—has emerged as a promising non‑invasive approach for cancer screening. For gastric cancer, methylation‑based assays and multi‑marker ctDNA panels are under development and early commercialization.

Why liquid biopsy matters: potential for high specificity, ability to detect molecular signals before morphological changes, and compatibility with routine blood draws.

Commercialization status: Several Chinese companies and international players are piloting or launching liquid biopsy screening products; regulatory approvals and real‑world performance data will determine uptake.

Breath Tests and Other Modalities

Breath tests analyzing volatile organic compounds (VOCs) and other non‑invasive modalities offer additional screening options. While promising, these technologies require further validation and standardization before large‑scale deployment.

China Gastric Cancer Screening Market – Regulatory and Reimbursement Environment

NMPA Approvals and Regulatory Pathways

Regulatory clearance from the National Medical Products Administration (NMPA) is a prerequisite for commercial distribution. Recent years have seen a faster review cadence for diagnostics, particularly for tests addressing major public health needs. Manufacturers pursuing gastric cancer screening tests must demonstrate analytical validity, clinical performance, and manufacturing quality.

Key considerations for manufacturers:

- Clinical validation in Chinese populations to demonstrate sensitivity and specificity for early‑stage disease.

- Post‑market surveillance plans to monitor real‑world performance.

- Quality management systems aligned with national standards.

Reimbursement Landscape

Reimbursement in China is complex and often province‑specific. National reimbursement lists (NRDL) and provincial procurement frameworks determine coverage for tests and services. For novel screening tests, inclusion in public programs or NRDL listings can dramatically accelerate adoption.

Strategies to secure reimbursement:

- Generate robust health economic evidence showing cost per life‑year saved or cost per cancer detected.

- Partner with provincial health authorities to run pilot programs demonstrating feasibility and impact.

- Engage payers early to align on evidence requirements and pricing expectations.

Guidelines and Clinical Pathways

National and specialty society guidelines influence clinician adoption. Inclusion of non‑invasive tests as recommended triage tools or as part of population screening algorithms will be a major inflection point for market growth.

China Gastric Cancer Screening Market -Competitive Landscape and Go‑to‑Market Strategies

Market Participants

The China gastric cancer screening market comprises a mix of:

- Domestic diagnostics companies developing serological, methylation, and ctDNA assays.

- International diagnostics firms partnering with local distributors or establishing joint ventures.

- Hospital groups and private health providers offering bundled screening packages.

- Technology firms providing AI and digital health platforms for risk stratification and reporting.

Commercial Strategies That Work

1. Evidence‑first commercialization Publish peer‑reviewed validation studies in Chinese cohorts and present real‑world pilot results to clinicians and payers.

2. Provincial pilot partnerships Work with provincial health bureaus to run screening pilots that demonstrate operational feasibility, detection yield, and cost metrics.

3. Integrated service models Offer end‑to‑end solutions: sample collection networks, centralized labs, digital reporting, and referral management to reduce friction for hospitals and screening programs.

4. Pricing and reimbursement alignment Adopt tiered pricing strategies for public programs versus private health packages; prepare health economic dossiers for NRDL or provincial reimbursement submissions.

5. Channel and distribution Leverage hospital networks, health management companies, and employer wellness programs to reach different segments of the population.

Mergers, Partnerships and Consolidation

Expect consolidation as larger diagnostics firms acquire niche technology providers to build comprehensive screening portfolios. Strategic partnerships between diagnostics companies and hospital groups will accelerate market penetration.

China Gastric Cancer Screening Market -Regional Adoption

High‑Incidence Provinces Lead Adoption

Provinces with historically higher gastric cancer incidence (e.g., parts of northern and eastern China) are often the first to pilot screening programs. These regions typically have stronger hospital infrastructure and more active public health budgets, enabling early adoption of new screening modalities.

Urban Private Market Growth

In major cities, private hospitals and health management companies offer premium screening packages that combine imaging, endoscopy, and advanced biomarker tests. These packages attract health‑conscious urban populations and corporate wellness programs.

Hospital Network Implementation

Large tertiary hospitals are integrating liquid biopsy assays into opportunistic screening for high‑risk patients (e.g., those with family history or prior H. pylori infection). These programs generate real‑world data and clinician familiarity, which in turn supports broader adoption.

China Gastric Cancer Screening Market -Implementation Considerations for Stakeholders

For Diagnostics Manufacturers

- Local validation: Prioritize multi‑center clinical studies in Chinese populations.

- Regulatory strategy: Engage NMPA early and design post‑market evidence plans.

- Quality and scale: Invest in manufacturing and lab capacity to meet provincial procurement demands.

- Partnerships: Collaborate with hospital groups and health bureaus for pilots and rollouts.

For Hospitals and Clinicians

- Clinical pathways: Define clear triage and referral algorithms that integrate new tests with endoscopy.

- Training: Provide clinician education on test interpretation and follow‑up protocols.

- Data systems: Implement digital reporting and patient tracking to ensure timely follow‑up.

For Payers and Policymakers

- Health economics: Evaluate cost‑effectiveness across screening strategies and prioritize models that maximize early detection while conserving endoscopy resources.

- Equity: Ensure rural and underserved populations are included in screening scale‑up plans.

- Quality assurance: Establish national standards for laboratory performance and reporting.

China Gastric Cancer Screening Market -Competitive Profiles and Company Spotlights

Domestic innovators are rapidly developing methylation and ctDNA assays tailored to Chinese genetic and epidemiologic profiles. These companies often combine laboratory services with digital reporting platforms to offer turnkey screening solutions.

International players bring validated technologies and global clinical evidence; they typically partner with local distributors or establish joint ventures to navigate regulatory and reimbursement pathways.

Hospital groups and private providers are important commercial partners. Hospitals that adopt screening tests early can become reference sites and generate the clinical evidence needed for broader adoption.

China Gastric Cancer Screening Market -Practical Roadmap for Market Entry

Phase 1 — Validation and Regulatory Preparation (0–12 months)

- Conduct multi‑center clinical validation in representative Chinese cohorts.

- Prepare NMPA submission and quality systems.

- Build health economic models tailored to provincial budgets.

Phase 2 — Pilot Deployment and Evidence Generation (12–24 months)

- Partner with one or more provincial health bureaus for pilot screening programs.

- Collect operational metrics: throughput, positive predictive value, endoscopy referral rates, and cost per cancer detected.

- Publish results and engage payers.

Phase 3 — Scale and Commercialization (24–60 months)

- Pursue NRDL or provincial reimbursement listings.

- Expand lab capacity and distribution channels.

- Offer integrated service models to hospitals and private health providers.

China Gastric Cancer Screening Market –Conclusion

The China Gastric Cancer Screening Market presents a compelling growth opportunity for diagnostics manufacturers, hospital systems, and health technology firms. The forecasted expansion from US$ 11,126 million in 2024 to US$ 16,597 million by 2033 reflects a market shaped by public health priorities, technological innovation, and evolving reimbursement frameworks. Success in this market will depend on rigorous clinical validation, smart regulatory and reimbursement strategies, and partnerships that align technology performance with real‑world implementation needs.

As China continues to invest in healthcare and adopt advanced screening technologies, the market is expected to play a crucial role in improving cancer detection and patient outcomes.

Frequently Asked Questions – China Gastric Cancer Screening Market

What is the current size of the China Gastric Cancer Screening Market?

The China Gastric Cancer Screening market is estimated at US$ 11,126 million in 2024 and is forecast to reach US$ 16,597 million by 2033 based on Frost & Sullivan projections.

Which technologies will drive growth in China Gastric Cancer Screening Market?

Non‑invasive technologies such as serological multi‑analyte panels, methylation‑based assays, and liquid biopsy ctDNA tests will drive in the China Gastric Cancer Screening market by enabling population‑level screening and efficient triage to endoscopy.

How important is NMPA approval for market access?

NMPA approval is essential for commercial distribution and public procurement. Manufacturers should plan robust clinical validation and post‑market surveillance to meet regulatory expectations.

Can liquid biopsy replace endoscopy for Screening?

Liquid biopsy is unlikely to fully replace endoscopy in the near term. The most practical model is a triage approach: use non‑invasive tests to identify high‑risk individuals who then undergo diagnostic endoscopy.

How should companies approach reimbursement?

Engage payers early, run provincial pilots to generate local evidence, and prepare health economic dossiers demonstrating cost‑effectiveness and budget impact.